Nobody cares about yield

As crypto turns every app into a bank, customers will decide where to deposit based more on rewards points than basis points

Crypto is turning every app into a bank. Stablecoins, blockchains, and DeFi have made it possible for any consumer platform to accept customer deposits and earn yield on them for a fraction of the cost and effort of a bank. Whop recently launched Whop Treasury, powered by Aave, giving users up to 6% yield on funds held on platform. Offering T-bill interest rates isn't new - you can get ~3.5% yield on a dozen different personal finance apps or just by holding USDC in a wallet - what's new is that consumer apps can now do it too.

When every consumer app can offer competitive yields, the hard part isn’t holding deposits - it’s giving customers a reason to deposit with you over the alternatives.

Valuable rewards, not competitive yields, are what actually motivate consumers to choose where to spend today. The same logic extends to where they’ll deposit funds, too.

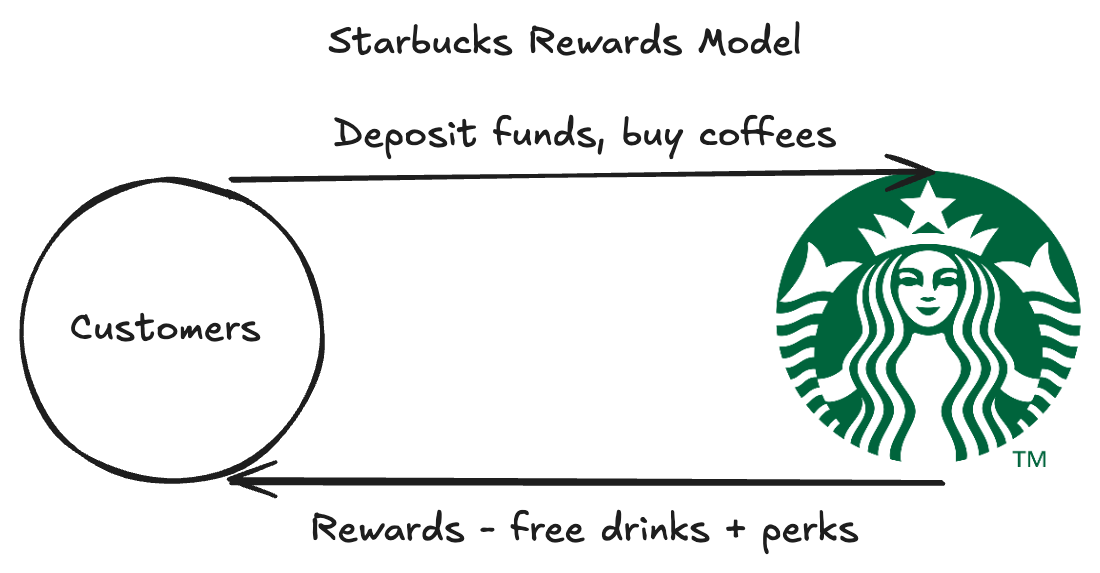

Case in point: Starbucks earns ~$100M in interest income by holding $1.8 billion in customer deposits through the Starbucks Rewards program and shares exactly 0% of that yield with its 32M members.

In a world where every app becomes a bank competing for share of wallet, customers will decide where to deposit based more on rewards points than basis points. A free drink, exclusive access to a lounge, and a membership status badge that build emotional loyalty are dollar-for-dollar more powerful than any interest rate.

The competition for the $11+ trillion US consumer deposits market is no longer limited to banks and fintechs. Any consumer platform with a valuable audience can now compete for share of wallet - and the ones that capture it won’t be the ones offering the best yield. They’ll be the ones offering the best rewards through their loyalty programs.

Why most loyalty programs fail

Most loyalty programs fail because they're a zero-sum game - every reward comes out of the brand's own pocket. A free coffee is a real cost, a discount on a purchase is real margin gone.

That leaves most brands stuck between two bad options: be too generous and lose money, or hold back and fail to motivate anyone to spend.

The result? Brands collectively spend tens of billions on loyalty programs that don't move the needle:

The average American belongs to over 17 loyalty programs and actively uses fewer than half.

$10 billion in earned rewards sits unclaimed every year because nobody cares enough to redeem them.

Starbucks Rewards pulls it off because coffee is a daily habit and ritual - their customers are in-store five times a week. Most businesses don’t have that kind of frequency working in their favor. If you run a DTC brand, a restaurant chain, or any business that isn’t a daily ritual, you need a way to offer rewards that actually motivate your customers - without destroying your own margins.

How Amex cracked the code

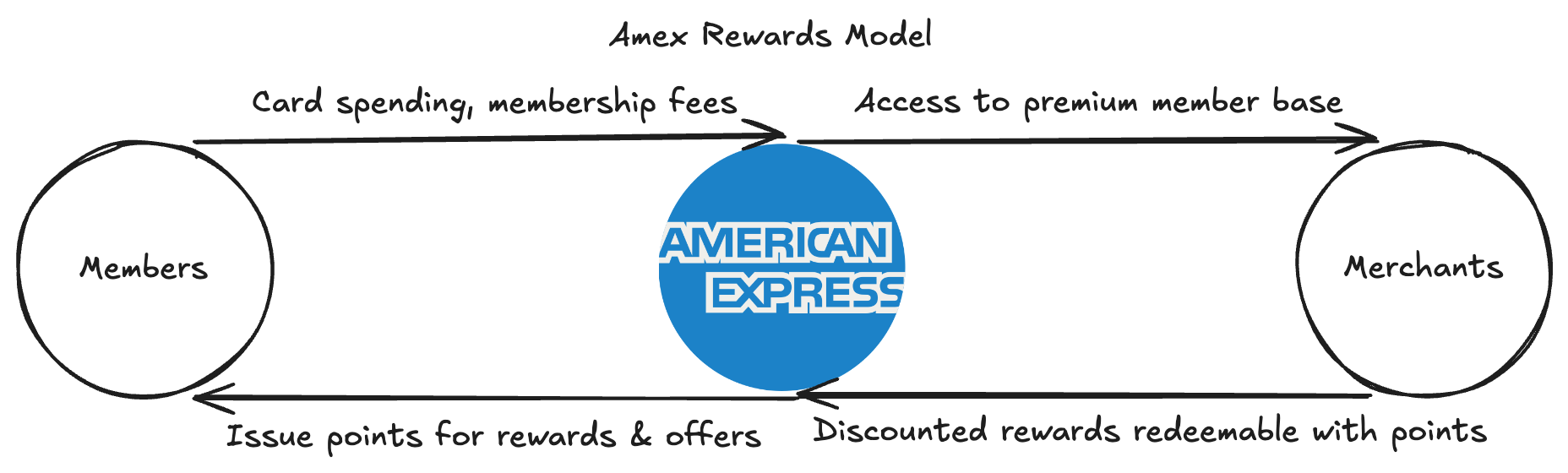

American Express figured this out decades ago, and built a $17 billion loyalty rewards network that members pay $10 billion a year in membership fees to access.

Here’s how it works: Amex doesn’t offer members rewards directly. They offer members a points currency that can be spent on rewards from hundreds of external merchants - airlines, hotels, retailers, restaurants, etc.

Members earn points for spending on their Amex card. They redeem those points for products and experiences from partner merchants. And the partner merchants accept those points as payment because it gives them something they can’t get anywhere else: direct access to Amex’s premium customer base.

In exchange for that access, partners offer wholesale pricing - which means Amex can deliver rewards worth $500 in value to a member for $200 in actual cost to the program.

It’s a three-way value exchange:

Members get rewards worth caring about

Partner merchants get access to high-value customers they’d otherwise pay a fortune to reach (e.g. via advertising)

Amex sits in the middle, delivering premium rewards at a fraction of what they’d cost to buy at retail.

Why most businesses can’t be Amex

So why doesn’t every business do this? Two structural barriers have kept the Amex model locked behind the balance sheets of the world’s largest companies.

It’s technically brutal to setup. Running this infrastructure requires dedicated engineering, security, and operations teams just to keep it working. Every external partner integration is a custom engineering project - stitching together different databases, product catalogs, inventory systems, and financial rails so they can talk to each other in real time. And because points are effectively real money, the stakes are high. A bug in the points ledger, a reconciliation error, or a security hole isn’t a minor inconvenience - it’s a direct financial loss, or worse, members exploiting the system and draining the program.

It’s capital-intensive and risky to run. Every point a brand issues is a future obligation - real money owed to a customer when they eventually redeem. That creates a massive ongoing liability on your balance sheet that has to be reserved against, managed, and hedged. Miscalculate redemption rates, partner pricing, or reward costs and you can find yourself underwater on a promise you've already made to millions of members. Running this safely requires treasury expertise, actuarial modeling, and capital reserves that most businesses simply don't have.

These are structural barriers, not effort problems. The only companies that have successfully pulled off an external partner rewards network at scale are the major credit card and airline loyalty programs - and it took them decades of relationship-building, dedicated partnership teams, and the balance sheet of a major F500 corporation to get there.

Until now.

Stablecoins are modern programmable points

The same onchain infrastructure that lets any app become a bank (like Starbucks) also enables them to turn their loyalty points into a real currency (like Amex).

The unlock is simple: instead of inventing a custom points currency, brands back every point with a stablecoin like USDC under the hood.

Members still see branded points in the app - nothing changes for them. What changes is what those points actually are.

Today, points programs are private currencies that only exist inside a single company’s database. That’s why connecting them across companies is so hard - every partnership is a custom engineering project because no two programs speak the same language. For a points currency to work across brands, it needs three things:

A stable value so partners know what they’re being paid

A shared standard so any merchant can accept it without custom integration

Broad distribution so it actually reaches partners where they do business.

USDC checks all three. It’s a fully-reserved digital dollar redeemable 1:1, runs on open blockchain rails any merchant can accept, and as the second-largest stablecoin in the world is already accepted by millions of merchants.

The capital problem disappears for the same reason. When every point is backed by a real dollar sitting in the treasury at the moment of issuance, there’s no floating liability to miscalculate, hedge, or reserve against. And because those dollars are held in USDC, the reserves earn USDC rewards (~3.5% at time of this writing). Points go from a liability on a brand’s balance sheet to a self-funding asset that gets cheaper to run as the program grows.

USDC, in this context, is a modern programmable reward point: stable, widely accepted, and built on open rails. Any brand can now use it to run the two most powerful loyalty models in consumer commerce - Starbucks and Amex - without the balance sheet, engineering team, or decades of partnership building it used to require.

Try the demo

To demonstrate this model in action I built a working demo using Coinbase Developer Platform and Claude Code for a hypothetical coffee brand (“Claude Code Coffee”).

The onchain loyalty platform is a three-sided marketplace: a consumer loyalty app, a merchant partner portal, and a brand admin dashboard. Here’s how it works in practice.

Consumer app

Sign-up: Users sign up with email or SMS. A crypto wallet is created automatically and invisibly under the hood using CDP Embedded Wallets.

Earning: Members earn points four ways: depositing funds via Apple Pay through Coinbase Headless Onramp, spending with the brand using Rain stablecoin cards, creating brand-approved user-generated content, and referring new members.

Rewards: Members redeem points for rewards from the brand itself and from approved partner brands at exclusive rates, with payments settling instantly for <$0.01 per transaction.

Brand admin portal

Dashboard: Brands manage the entire program from a single dashboard - analytics, member CRM, rewards, merchants, analytics, and program economics.

Deal review: The Amex negotiation that takes dedicated teams and months of back-and-forth happens here in minutes: When a partner submits a listing, the brand reviews it through an interactive deal tool - adjusting the discount, setting the budget, choosing which tiers get access, and watching in real-time how the deal compares to other active partnerships.

Partner merchant portal

Campaigns: Partners apply, list products at wholesale prices, and manage their campaigns through a self-serve dashboard.

Payouts: Partners see every redemption settled instantly in USDC on Base, paid out for less than a penny in fees, with no invoicing, 60-day cycles, or inventory management.

What’s next

Loyalty AI agent: Making sure teams of any size can operate a world-class onchain loyalty program as easily as they can create it - by building an AI agent that runs the program as analyst, treasurer, partnerships lead, and buyer all at once,

Shopify integration: Plugging into the merchant network where every one of Shopify's 5.5 million merchants is already USDC-enabled through the Universal Commerce Protocol pioneered by Coinbase and Shopify, and agentic-ready through Shopify’s new AI Toolkit.

Why now

The most valuable consumer companies in the world sell commodities but operate like banks. Their loyalty programs are the software that makes it possible.

Starbucks sells coffee you can get anywhere - and earns $100 million a year in interest on $1.8 billion in customer deposits sitting in their app. Airlines would be unprofitable without their loyalty programs. Amex doesn't sell a product at all - they sell access to buy other products, and their rewards network is worth tens of billions.

The actual asset these companies are built on is the customer relationship. The loyalty program is the software that captures its value.

Until now, building that software required a hundred-million-dollar balance sheet and decades of partnership infrastructure. Stablecoins and onchain rails change that - any brand can now build it themselves.

That means any business can measure and capture the value its brand is already sitting on. Brands don’t just win deposits - they own the customer relationship outright, capture first-party data directly, lower customer acquisition costs, and reward their best customers in ways that actually move behavior.

Not every business will become the Amex or Delta of its category. Early movers will set the standard and capture the most valuable customers in their segment. Many others will participate as partner merchants - a meaningful customer acquisition cost improvement over the exploding cost of social ads. But the deposits, the data, and the compounding relationship belong to the brand running the program.

If you’re a brand or business interested in building a loyalty program of your own, try the demo and reach out. I’d love to walk through what a deployment could look like for you. I lead loyalty partnerships on the Base BD team at Coinbase, and previously helped design the loyalty program at Dunkin’.